Debt Markets Diverge From AI Stock Market Optimism

Artificial intelligence equities have continued to surge, driven by optimism around automation, cloud computing, and generative AI adoption. Stock investors appear willing to overlook warnings of overvaluation as long as growth narratives remain intact.

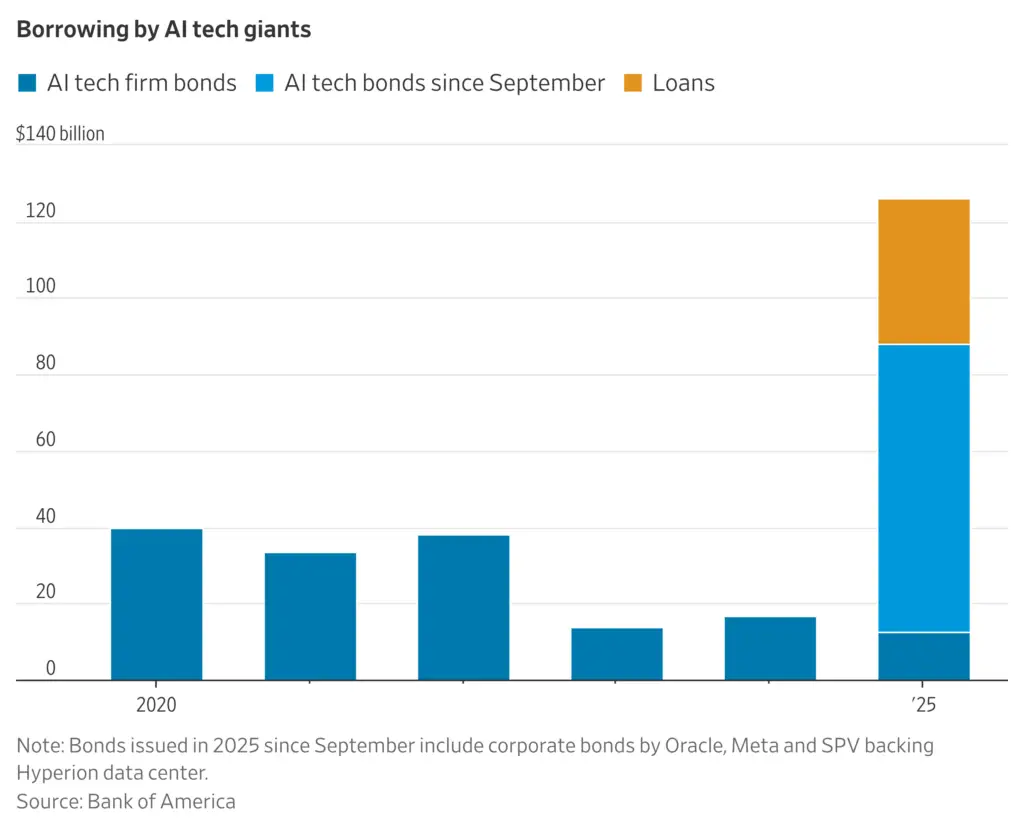

Debt investors, however, are responding far more cautiously. As AI companies raise billions to fund infrastructure and expansion, lenders are demanding significantly higher interest rates to compensate for elevated financial risk.

Rising Borrowing Costs Expose Credit Market Skepticism

New AI-focused borrowers are paying notable premiums compared with similarly rated firms in traditional sectors. In several recent deals, interest rates exceeded benchmarks by wide margins, reflecting lender unease.

This divergence signals skepticism about whether young AI firms can deliver predictable cash flows. Debt markets are effectively pricing in uncertainty around timelines, profitability, and long-term demand sustainability.

Infrastructure Spending Creates Revenue Timing Risks

Many AI companies depend on massive data center projects that require extensive upfront investment. These facilities often take years to construct before generating meaningful leasing or service revenue.

Any construction delays can push revenue recognition further into the future. Debt investors worry that prolonged buildouts could strain liquidity before cash flows stabilize.

Recommended Article: 2026 Artificial Intelligence Trends Redefining Business, Leadership, and Work

Customer Concentration Raises Structural Vulnerabilities

Several AI infrastructure providers rely heavily on contracts with a small number of hyperscale clients. While these agreements offer credibility, they also concentrate revenue risk.

If a major client scales back demand or renegotiates terms, financial stability could weaken quickly. Ratings agencies now closely examine customer diversification when assessing AI creditworthiness.

Credit Ratings Highlight Uneven Risk Distribution

Established technology firms continue to borrow at favorable rates due to strong balance sheets and diversified income streams. In contrast, newer AI players often fall into speculative-grade credit categories.

These lower ratings reflect uncertainty rather than immediate distress. Higher yields compensate investors for the possibility that growth projections may fail to materialize as expected.

Equity Optimism Clashes With Debt Market Discipline

Equity investors benefit from unlimited upside if AI adoption accelerates globally. This dynamic encourages greater tolerance for volatility and long-term experimentation.

Debt investors operate under different incentives. Without upside participation, lenders focus on downside protection, repayment certainty, and asset durability.

Implications for the Future of AI Investment

Rising borrowing costs may slow the pace of AI infrastructure expansion. Companies facing tighter financing conditions could delay projects or seek alternative funding structures.

Over time, this discipline may strengthen the sector by rewarding sustainable business models. Firms capable of generating steady cash flows are likely to endure, while weaker players face consolidation or exit.