The Rise and Fall of the Bitcoin Treasury Boom

The once-celebrated Bitcoin treasury strategy is now under severe strain as falling prices expose structural weaknesses in the model. More than 200 public companies accumulated large Bitcoin reserves during the 2025 rally, betting on perpetual appreciation.

At the peak of enthusiasm, firms issued shares and low-cost debt to acquire additional coins. As Bitcoin surged toward $126,000, the strategy appeared self-reinforcing, allowing companies to leverage rising valuations to expand holdings further.

Premiums Turn Into Discounts

A central metric in the treasury trade was market-to-net-asset value, or mNAV, which measures how much investors pay for exposure relative to underlying holdings. During euphoria, some firms traded at multiples of their Bitcoin reserves.

When Bitcoin reversed course, those premiums collapsed into steep discounts. Investors began questioning why they should pay for indirect exposure when direct ownership or exchange-traded funds offered cleaner alternatives.

Shareholder Revolts Emerge

Several companies have faced open dissent from investors demanding drastic changes. In one high-profile case, a major shareholder called for management resignations and liquidation of the company’s Bitcoin holdings.

Such activism reflects frustration with unrealized losses and declining stock prices. As share values sink below the net worth of underlying digital assets, pressure mounts to unlock capital rather than maintain long-term crypto exposure.

Forced Sales and Buyback Plans

One publicly traded firm recently approved the potential sale of thousands of Bitcoin to fund a share repurchase program. The move effectively reverses the original thesis of accumulating digital assets as a growth engine.

Selling Bitcoin to stabilize equity valuations contradicts the treasury model’s core premise. Instead of leveraging rising crypto prices to boost stock performance, companies are now liquidating assets to contain damage.

Strategy Dominates Corporate Buying

Amid the turmoil, one company stands apart: Strategy, formerly known as MicroStrategy. Led by executive chairman Michael Saylor, the firm remains the largest corporate holder of Bitcoin.

Even so, Strategy’s stock has experienced extreme volatility and heavy short interest. The company’s dominance highlights how capital has concentrated in a single flagship player as smaller treasury firms falter.

Structural Weaknesses in the Model

Analysts argue that the treasury strategy depended heavily on sustained price appreciation. When Bitcoin rallied, leverage amplified gains and attracted new investors seeking equity exposure to crypto upside.

However, leverage works in reverse during downturns. Falling prices magnify losses, erode investor confidence, and reduce access to capital markets, creating a self-reinforcing downward spiral.

Outlook for Corporate Crypto Holdings

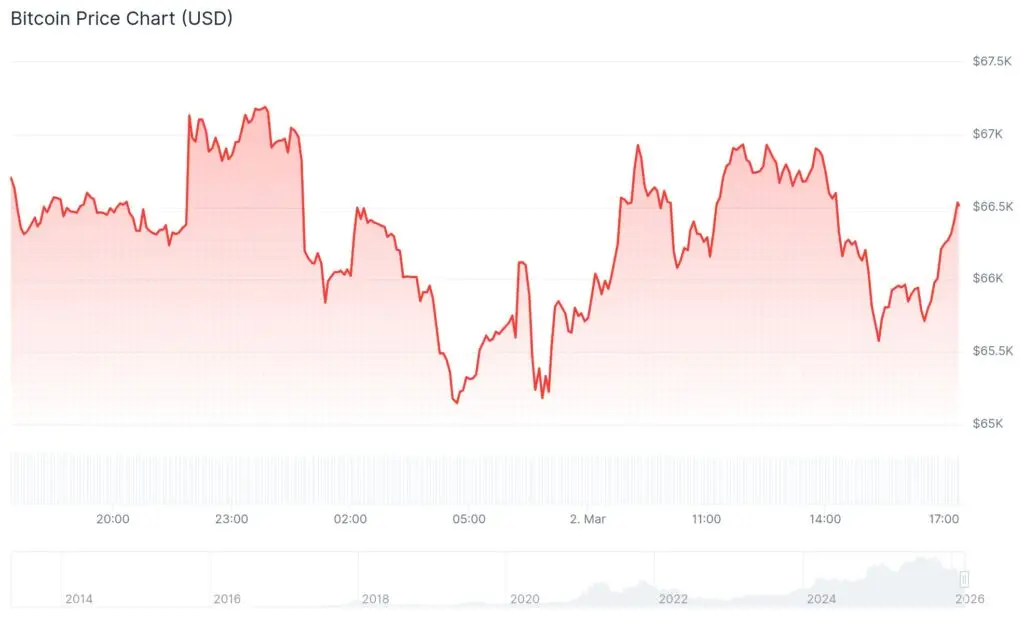

With Bitcoin trading roughly 50% below its late-2025 highs, many treasury companies sit on substantial unrealized losses. The sector’s combined holdings are now valued far below their peak.

Future performance depends largely on whether Bitcoin can regain momentum. Until then, the unraveling of the treasury trade serves as a cautionary tale about leverage, timing, and the risks of anchoring corporate strategy to volatile digital assets.